You feel inflation at the supermarket long before you read about it in the news. A trolley that ran you $200 a year ago is closer to $206 now. That might not seem like much, but the increased power bill, the higher insurance renewal, and the rent increase quietly add up.

That's inflation, and after a few quiet years it's back near the top of the agenda. New Zealand's annual rate hit 3.1 percent in early 2026, a notch above the top of the Reserve Bank's 1 to 3 percent target band.

As an economic headline it's easy to tune out. For your own money, though, it's personal: a slow tax on every dollar you're holding in cash. So here's the quick version of what it is, why it bites harder than it looks, and what you can do about it.

What inflation really is

Strip the jargon, and inflation is just prices going up, which is the same thing as your dollar buying less than it did.

Stats NZ keeps score by pricing a basket of the stuff we all pay for: the weekly shop, rent, power, petrol, the insurance bill. If the cost of that basket is up 3 percent on a year ago? Then inflation is 3 percent. That's how it's calculated.

What's driving it

Knowing the definition is one thing. The more useful question is what pushes those prices up in the first place, because that tells you whether a spike is the kind that sticks around or blows over.

It comes down to two engines.

The first is demand: when households and businesses all want to spend at once, and there isn't enough to go round, sellers can raise prices and still make a sale. Cheap borrowing, government spending and a hot housing market all pour fuel on that.

The second is cost: when the things behind a product get dearer, the price tag follows. A jump in global oil prices, shipping costs that suddenly triple, higher wages, or a weaker Kiwi dollar quietly make almost every product and service more expensive.

The 2021 to 2022 surge was a textbook mix of both. It started on the demand side, with rock-bottom interest rates, pandemic support payments and a booming property market driving up demand.

Then the supply side piled in: closed borders choked off workers, global shipping snarled up, and the war in Ukraine sent fuel and food prices flying. Two engines running at once is why the number climbed so fast.

There's a quieter driver too: expectations. If people simply assume prices will keep rising, they ask for bigger pay rises and set higher prices on their products and services to stay ahead. The expectation of inflation makes itself come true.

Breaking that loop is the main job of the Reserve Bank, which aims to keep inflation near 2 percent. Its main lever is the Official Cash Rate, sitting at 2.25 percent right now: when prices run hot it holds or lifts rates to take the heat out of demand, and when things cool it can cut. You don't need to track any of that week to week, but it's why the interest on your savings rises and falls the way it does.

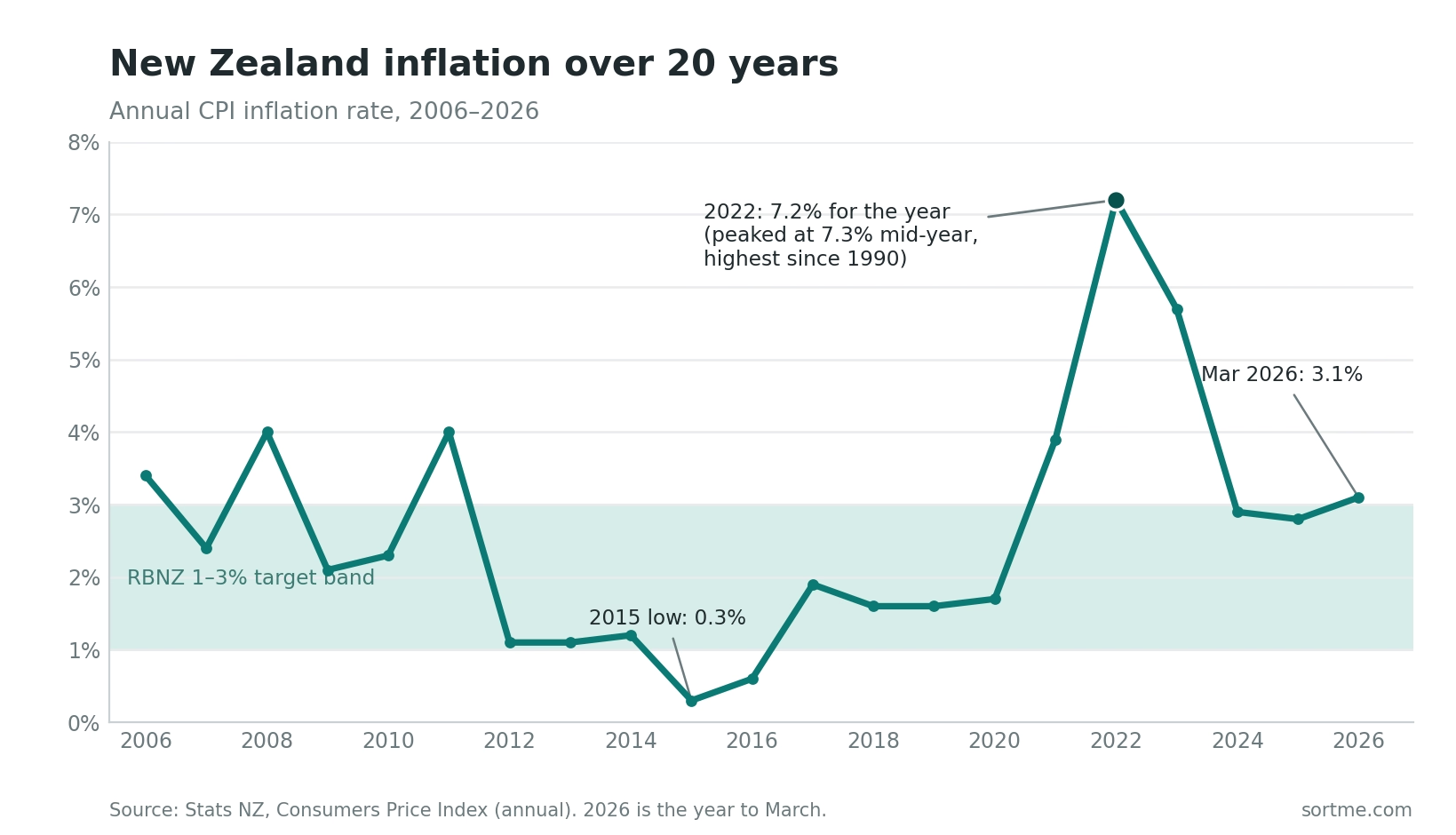

Inflation over the last 20 years

Today's 3 percent can read as alarming or completely normal depending on what you hold it up against.

For most of the last two decades it was the latter. Through the 2010s inflation mostly sat inside the Reserve Bank's 1 to 3 percent band, and in 2015 it nearly disappeared, averaging just 0.3 percent for the year. The exception was the post-pandemic spike, which peaked at 7.3 percent in mid-2022, the highest New Zealand had seen since 1990. It has since dropped back close to where it usually lives.

Two things jump out. Even the calm years never quite reached zero, so idle cash was losing a little ground the whole way through. And the climb from under 2 percent to over 7 in about eighteen months shows how fast the picture can turn, usually with very little warning for anyone sitting on cash.

Why it quietly eats your savings

Here's the part that catches people out. The price tags climbing is only half of it. The sneakier half: the cash already in your account buys a bit less every year, even while the balance on screen never budges.

Picture $10,000 parked in a typical everyday account at 0.10 percent. A year on, it's made you about ten dollars. Meanwhile, with inflation near 3 percent, you now need roughly $10,300 to buy what that $10,000 bought last year. Same number on the screen, yet you've quietly slipped about $300 behind. Leave it five years and that gap stops being pocket change.

This is the difference between a nominal return (the number on the statement) and a real return (what's left after inflation). A savings account paying 0.10 percent while inflation runs at 3 percent is handing you a negative return of roughly minus 2.9 percent. You don't feel like you've lost anything because the balance never drops. What's lost is the buying power of those dollars.

The trap is that the default everyday and "on call" savings accounts at the big banks pay almost nothing: some sit at 0.10 to 0.40 percent interest. If you've never made an active choice about where your cash lives, that's probably where it is, and it's going backwards.

How to stay ahead of it

Staying ahead of inflation isn't complicated. The goal is simple: don't let money sit somewhere that pays less than prices are rising. A few moves do most of the work.

Get your cash off the floor. The easiest win is moving cash out of a near-zero everyday account into something that at least keeps pace with inflation. High-interest savings accounts and PIE savings funds in NZ are paying around 3 percent in 2026, which roughly holds the line against inflation rather than losing to it. We wrote a full guide to exactly where to put it, with live rates, in Your default savings account is leaking money: where to park cash in NZ. Start there if your everyday balance is bigger than a couple of weeks of bills.

Match the timeframe to the home. Money you need this week stays in your everyday account, and that's fine. Money you won't need for a few months can earn more in a savings fund or a high-interest savings account. The point isn't to chase the highest number, it's to stop holding more cash than you need at a rate that loses to inflation.

For long-term money, you need growth, not just safety. Keeping pace with inflation protects your buying power. Getting ahead of it, over years, usually means owning assets that grow faster than prices: shares, index funds, and the KiwiSaver most Kiwis already have. Historically, a low-cost index fund has beaten inflation by a comfortable margin over the long run, which is the whole point of investing money you won't touch for years rather than letting it sit in cash. Just be honest about timeframe: that's for money you can leave alone, not your emergency buffer.

Keep your buffer, then put the rest to work. None of this means emptying your bank account. Hold your emergency fund and short-term spending in cash where you can reach it. It's the surplus sitting idle, beyond what you really need on hand, that inflation feeds on.

Where SortMe fits

The reason inflation gets away on people is that the idle cash is invisible. It's spread across a few accounts, none of them obviously a problem, so nobody adds it up.

SortMe puts every account in one view, so you can see the full cash pile as a single number instead of a balance hiding in each bank app.

The Cashflow Health Score flags when you're holding more cash than your spending needs, which is the exact money inflation is eroding. And because you can watch your net worth over time, you start to see the real story: whether your money is genuinely growing, or just standing still while prices move on without you.

Get ahead of it

The cash quietly losing ground to inflation is usually the cash you've stopped looking at. SortMe pulls every account into one view, flags the idle money going backwards, and shows whether your net worth is genuinely growing or just standing still against rising prices.

Join the 12,000+ Kiwis already getting ahead of it. Start a 7-day trial for $1, and if SortMe doesn't find you $500 of savings in your first 30 days, you get your money back.

This article is general information, not personalised financial advice. What's right for you depends on your own situation. If you'd like advice for your circumstances, talk to a licensed financial adviser.