You open your bank app on payday. $6,400 sitting in the current account. For about three seconds, you feel fine.

Then you remember the rental mortgage is at a different bank. Your partner's KiwiSaver is at a third. The joint savings have been drained again and you can't remember why. Last month, without noticing, your household spent another $1,100 on takeaways and subscriptions you'd forgotten about. The figure on the screen tells you nothing you can act on.

If this is you, you don't have a budgeting problem. You have a visibility problem. And the app from the bank you signed up with at nineteen is never going to solve it — because it can only see itself.

This guide is for the group of NZ households that have already outgrown that setup. Three bank accounts. Two KiwiSavers. A rental mortgage on one bank, the main mortgage on another. Sharesies, Hatch, a credit card, a wedding still being paid off. You're typing “budgeting app NZ” into Google because spreadsheet Sunday isn't working and the bank app isn't enough.

Open banking went live across New Zealand in 2025(1). It changed what a budgeting app can actually do. For the first time, one app can see every major NZ bank account, every major KiwiSaver provider, and the rest of a household's money, all with your consent and none of your passwords.

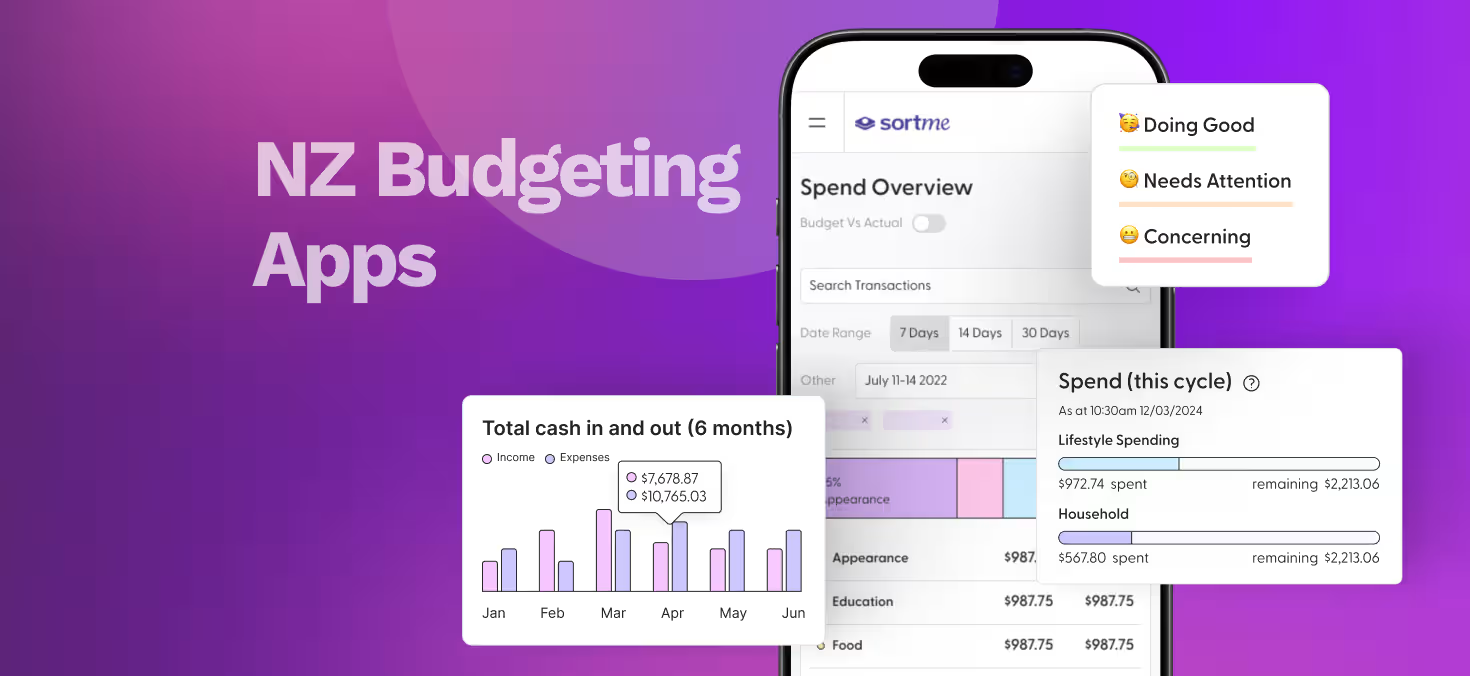

SortMe is the NZ-built app designed for households who've outgrown one bank. This article covers what a NZ budgeting app has to do in 2026, why SortMe was built for exactly this household, and how it compares to the alternatives.

“Most of the budgeting apps NZ households start with only see one bank. That's fine if you run everything through one account. It's not fine if you're like most of our users — three bank accounts, two KiwiSavers, a rental mortgage on one bank, the main mortgage on another. SortMe was built for this modern financial complexity.”

— Carl Thompson, Founder & CEO, SortMe

Why single-bank apps stop working once you've outgrown one bank

The standard failure is the same every time.

Rent leaves one bank. Power leaves another. KiwiSaver goes nowhere visible — it's deducted at the payroll level before you see it. Rental income lands at a third bank. Each stream is a slice of the picture. No bank app you already have will combine them.

The usual workaround is a spreadsheet updated by hand. It works for a fortnight. Then someone forgets a new standing order, categories drift, and the sheet falls a week behind. Every SortMe user we've spoken to who arrived from a spreadsheet said the same sentence: “I was spending a Sunday a month on this and it was still wrong.”

The other workaround is the single-bank apps themselves — ANZ goMoney, ASB Track my Spending, BNZ's dashboard, Westpac's. Each does its one job well. None of them see the other banks, and none see Sharesies, Kernel, Booster, or Hatch. A household with accounts across four institutions gets four partial views and no complete one.

What a NZ budgeting app has to do in 2026

Three things. Non-negotiable.

Connect to every major NZ bank in one place. SortMe connects to every major NZ bank (ANZ, ASB, BNZ, Westpac, Kiwibank, Co-op, Heartland, SBS), plus KiwiSaver providers, investments via Sharesies and Hatch, and your credit cards. Connections run through Akahu(2), New Zealand's regulated open-banking data provider, so your bank credentials never touch SortMe's servers. Data flows on the same consent-based pipes NZ's open banking framework was built on.

Categorise everything automatically. A useful budgeting view is not a transaction list. It's “you spent $1,240 on groceries this month — $190 more than last month,” across every account you own. Manual categorisation across four banks is a part-time job, so it has to be automatic. SortMe reads the merchant name, amount pattern, and account type and categorises without you touching it. Fix one it gets wrong, and it learns.

Produce one view of the household. Your real net worth is not what sits in your ANZ accounts. It's your accounts plus your KiwiSaver plus your investments plus your property values, minus your mortgages and any other debt. An app that can't combine those into one number isn't giving you a household view — it's giving you a fragment. SortMe tracks net worth live and runs the SortMe Cashflow Health Score across the whole household, not one account at a time.

What SortMe users see on day one

The first screen after connecting shows three things:

- Current net worth, compiled from every account SortMe can see

- Today's Safe to Spend figure — the amount available to spend without dipping into money allocated for bills, savings, or goals

- The categories you actually spent in last month, ranked by size

Most people hit two surprises in that first view. One is a category they had no idea was that big — almost always subscriptions or takeaways. The other is that their real net worth is different from what they thought, usually because a KiwiSaver or a mortgage had been quietly missing from their mental sum.

Both surprises pay off. The subscription one often covers the cost of SortMe itself on day one — the app flags unused subscriptions and recurring charges that slip through. The net worth one shows up in conversations with accountants, advisers, and mortgage brokers.

On average, SortMe users find $2,371 a year in savings they didn't know they had.

What's included

SortMe is one simple subscription. No tiers. No upsells.

Every plan includes:

- Connections to every major NZ bank, plus KiwiSaver providers, Sharesies, Hatch, and credit cards

- Automatic transaction categorisation across every account

- Live net worth tracking across the whole household

- Smart budgeting and Safe to Spend

- Spend reports and insights

- Subscription management — find and cancel what you don't use

- Goal tracking

- AI-powered recommendations

- Sassy Susan, SortMe's in-app AI cash coach

- A free 30-minute session with a SortMe Pro

- The SortMe Cashflow Health Score

Pricing

- $1 for your first 7 days. A paid trial — a dollar in, full product out, cancel anytime.

- $29/month month-to-month, or $99/year on the annual plan (save 60%).

- 30-day money-back guarantee. If SortMe hasn't helped you feel more confident and in control of your money in the first 30 days, you get a full refund.

The NZ budgeting app landscape

A few apps people ask about.

PocketSmith. NZ-built, around since 2008, deepest cashflow forecasting on the market. If you want 30-year projections and are comfortable with a busier interface, PocketSmith is designed for that level of complexity — built for the home accountants. SortMe is sharper and more automated. For a cleaner day-to-day view, the NZ advisor pathway, and a Cashflow Health Score over raw numbers, SortMe is the better fit.

MyBudgetPal (built by Booster). Free and well-made for first-time NZ budgeters. A cleaner entry point than a spreadsheet. Doesn't match SortMe on multi-bank depth, the advisor network, or the net-worth view. Users are moving across to SortMe as the gaps show.

Bank apps (ANZ goMoney, ASB Track my Spending, BNZ's dashboard). Single-bank by design. If you only use one bank, you likely don't need a separate budgeting app.

Sorted (sorted.org.nz). Not affiliated with SortMe. A financial-literacy service, not a budgeting app. Excellent for calculators and concepts. Not a live household view.

Security and data practice

Two things worth knowing.

Bank credentials are not stored by SortMe. Connections run through Akahu using NZ's open-banking consent framework — you authorise with your bank directly, SortMe receives read-only data, and you can revoke the connection at any time.

SortMe does not sell user data. Ever. That's one of the four non-negotiable principles the company was founded on(3), and it's written into the terms.

What to check before you pick a NZ budgeting app

Six questions. If the app you're considering can't answer all six, it was built before open banking landed properly in NZ.

- Does it connect to every NZ financial institution you actually use?

- Does it see your KiwiSaver alongside your bank accounts?

- Does it categorise automatically, or does it want you to tag everything manually?

- Is there an advisor or broker pathway when you're ready for one?

- Who handles the open-banking connection? (Akahu is the NZ standard.)

- What happens to your data if you cancel — is it deleted?

The practical next step

The fastest way to know whether a multi-bank budgeting app is worth it is to connect two banks and watch the categorisation for a week.

SortMe is $1 for your first 7 days. If Safe to Spend and the category breakdown haven't shown you something useful inside that week, cancel — nothing else spent.

If they have, you're looking at $29/month, or $99/year on the annual plan (save 60%). Less than the takeaways SortMe is about to help you stop forgetting about.

Start at sortme.com. Connect two banks. See what appears.

Sources

- Open Banking Is Finally Live in NZ, SortMe Blog

- Akahu — New Zealand's Open Banking Platform, Akahu

- About SortMe, SortMe